About

Apple (AAPL), as a company, creates a wide range of consumer electronic gadgets, which encompass smartphones (known as iPhones), tablets (referred to as iPads), personal computers (like the Mac), smartwatches (the Apple Watch), and AirPods, among other offerings. Furthermore, Apple provides various services to its customers, such as Apple Music, iCloud, Apple Care, Apple TV+, Apple Arcade, Apple Fitness, Apple Card, and Apple Pay, just to name a few. Apple’s products not only involve in-house developed software and semiconductors but are also well-known for their seamless combination of hardware, software, semiconductors, and services. These products are available for purchase both online and in Apple’s own stores, as well as through other retail partners.

In this analysis, we will thoroughly examine Apple’s financial performance and explore its prospects for future growth. Our analysis will focus on how the company generates sales, its profitability, and its proficiency in handling cash flow. By gaining a more profound comprehension of these factors, you will be better prepared to make an informed choice regarding whether to invest in Apple.

Apple’s Strong Financial Performance and Brand Loyalty

Investing in Apple Inc. is a compelling choice due to its remarkable track record. Apple has consistently demonstrated financial stability, driven innovation in the tech industry, and been led by a visionary management team. This impressive history aligns well with your investment goals, making Apple a strong candidate for long-term growth and stability.

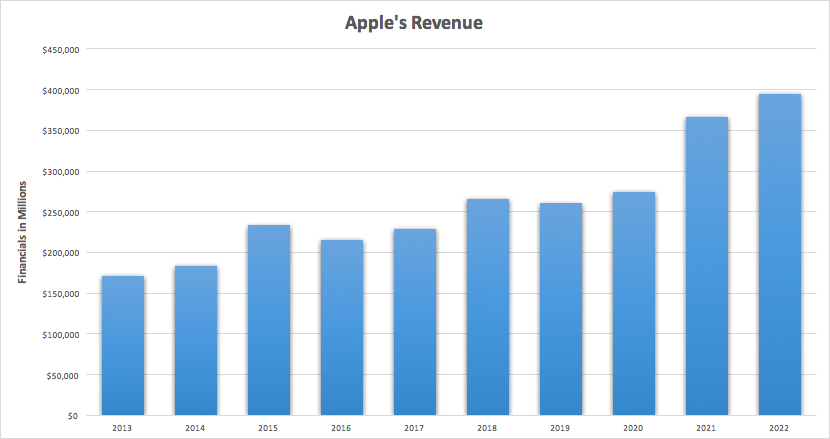

Over the past decade, Apple Inc. has exhibited a truly impressive track record of growth and financial success. From 2013 to 2022, Apple’s revenue has surged from $170.9 billion to a staggering $394.3 billion, representing a total growth of approximately 130.72%. This remarkable growth has translated to a compounded annual growth rate (CAGR) of about 8.72%, which is a testament to the company’s consistent ability to expand its market and product offerings.

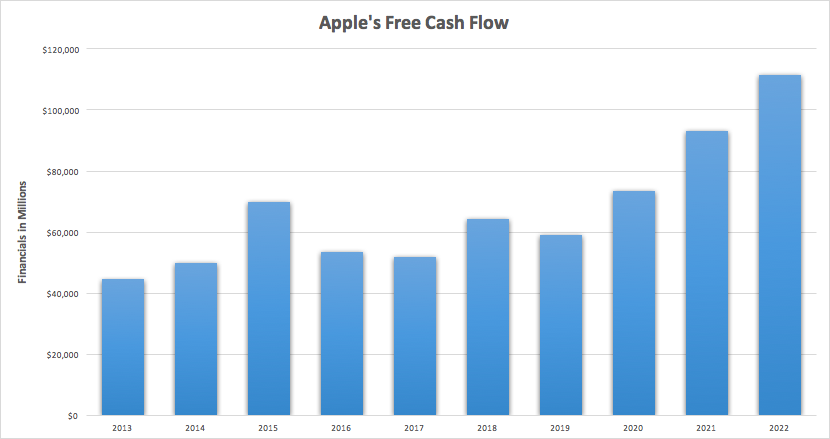

Additionally, Apple’s free cash flow has also seen substantial growth, increasing from $44.59 billion in 2013 to $111.44 billion in 2022. This growth in free cash flow highlights Apple’s strong financial position and its ability to generate significant cash from its operations. The CAGR for free cash flow over the same period is approximately 9.59%, reflecting the company’s efficient management of its resources.

These strong results on the top and bottom lines can be attributed to the company’s strong brand identity and customer loyalty. Over the years Apple has cultivated one of the most remarkable brand loyalties in the technology industry and beyond. Its dedicated customer base is a testament to the company’s ability to consistently deliver innovative, high-quality products and a seamless user experience.

Apple’s ecosystem, including its hardware, software, and services, creates a unique bond with users, fostering a sense of trust and loyalty that extends well beyond the purchase of a single device. This unwavering brand loyalty has not only contributed to Apple’s sustained success but has also established a model for other companies to aspire to in building enduring customer relationships.

It’s worth noting that according to Forbes, Apple currently holds the top position as the world’s most valuable brand. Their assessment places the value of the Apple brand at a remarkable $241 billion, reflecting a substantial 17% increase compared to the previous year. This data underscores the enduring strength and growth of the Apple brand.

Furthermore, Apple’s strong brand and customer loyalty have been instrumental in the company’s impressive profitability over time. Their ten-year average return on invested capital (ROIC) of over 28% and current ROIC of 39% showcase Apple’s efficient use of capital to generate profits, making it a financially robust and attractive investment choice. Additionally, the company’s remarkable earnings of $577,000 per employee, compared to the sector median of just $33,000, underlines the exceptional productivity of its workforce, demonstrating how these financial metrics provide valuable insights into Apple’s financial health and competitive advantage.

Charting Apple’s Path to the Future

Let’s look at Apple’s earnings outlook for the rest of fiscal year 2023. In terms of earnings per share (EPS) estimate for 2023, Apple is estimated to report EPS for of $6.19. Now, this represents a relatively modest year-over-year growth of 1.30%. While any growth is generally seen as a positive sign, this increase is not as substantial as some might have expected from Apple.

Moving on to the revenue estimate for 2023, it’s projected to be approximately $390.7 billion. However, there’s a noteworthy point here. The YoY (year-over-year) growth in revenue is expected to be negative, specifically at -0.90%. In other words, Apple’s revenue for 2023 is anticipated to be slightly less than in the previous fiscal year.

Looking ahead to 2024, Apple seems to be in a strong position. Their estimated earnings per share (EPS) is $6.74, showing an impressive 8.90% year-over-year growth. This suggests improved profitability and their revenue estimate for 2024 is $415.3 billion, with a positive 6.30% year-over-year growth. Overall, Apple’s outlook for revenue and earnings growth in the coming years appears to be pretty good.

Let’s delve into Apple’s strategy for maintaining its rapid growth in the coming years. A pivotal part of this strategy involves the development of new products and services, such as wearables and augmented reality devices. You see, critics have frequently scrutinized Apple’s heavy reliance on the iPhone.

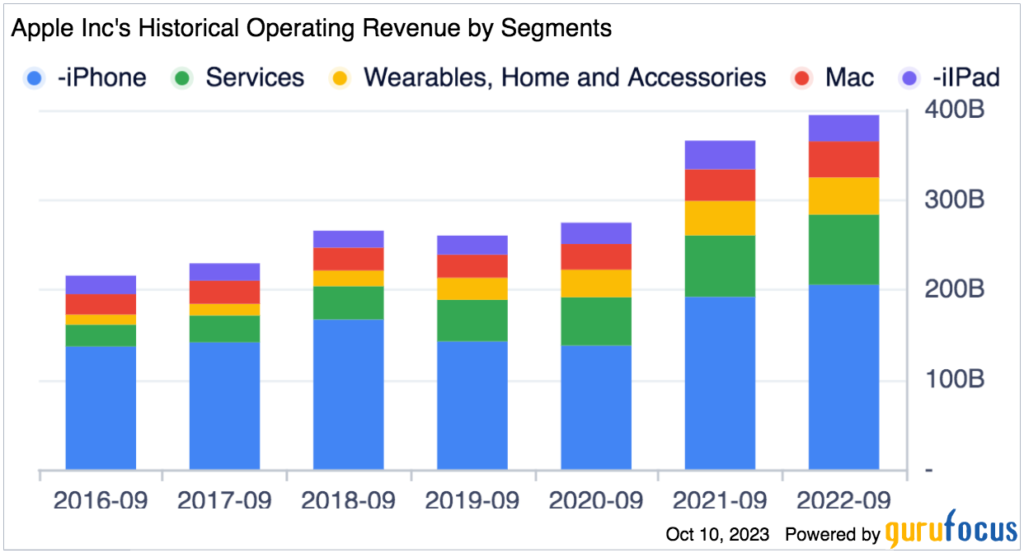

In the year 2022, the company managed to pull in an impressive $205 billion in sales from its iPhones, marking a notable 7% increase compared to the previous year. To put it into perspective, the iPhone continues to be Apple’s primary revenue driver, accounting for a whopping 52% of the company’s total sales.

iPhone sales have generally been on the rise, but there were a few years when they actually dropped. The latest iPhones haven’t wowed users like before because they mainly offer small improvements, like slightly better cameras and longer battery life. It seems smartphone tech is maturing, and people are getting used to these incremental changes instead of groundbreaking innovations. As technology in the smartphone industry reaches a more mature stage, it’s inevitable that iPhone sales growth will slow down. This underscores the importance for Apple to actively explore and cultivate other avenues for business growth.

On the other hand, Apple’s services segment had a strong showing in 2022, generating a substantial $78.1 billion in revenue. This represents a solid 14% year-over-year growth and contributed significantly, making up 19.8% of the company’s overall sales for the year. In Apple’s most recent earnings call, CEO Tim Cook reported that Apple now has over 1 billion paid subscriptions in it’s ecosystem.

It’s hard to wrap my head around having 1 billion paying subscribers but it is equivalent to approximately one-seventh of the world’s population actively using and paying for a particular service or platform, highlighting its immense global impact and reach. These subscriptions include for services like Apple Music, Apple TV+, iCloud storage, Apple Arcade, and other premium content and services offered by Apple.

The fact that Apple’s Services revenue hit an all-time high underscores the increasing importance of services as a revenue driver for the company. Apple has been strategically expanding its services portfolio to keep users within its ecosystem and generate recurring revenue. Paid subscriptions are a key part of this strategy, as they provide a steady stream of income.

This is an encouraging development for Apple, as high levels of paid subscriptions indicate that Apple customers are increasingly engaged with the company’s ecosystem of services. This engagement leads to greater customer loyalty and a more stable revenue stream for Apple.

While smart phones appear a maturing technology, Apple’s upcoming release of the Apple Vision Pro in early 2024 is generating quite a buzz. This product, as described by Apple, is nothing short of a marvel of engineering. It’s proudly touted as the ‘most advanced personal electronic device ever created.’ Now, that’s a big claim, isn’t it?

Justin Sullivan

The Apple Vision Pro is all about spatial computing. That might sound like a mouthful, but it’s a concept that’s reshaping how we interact with technology. It essentially bridges the gap between our digital world and the physical one. Imagine being able to reach into your digital space, interact with information, and explore content in three dimensions. It’s like a futuristic blend of our digital and physical realities.

Apple isn’t just releasing a product; they’re pioneering a technological frontier. They’re putting themselves at the forefront of this transformative technology, and that’s no small feat.

CEO Tim Cook seems pretty excited about it too. He mentions that the tech world has already had a taste of the Apple Vision Pro. Press, analysts, developers, and content creators have all given it a whirl, and guess what? They’re thrilled about it. Their enthusiasm tells us that Apple has created something that’s not only impressive but also generating a ton of interest and attention in the tech community.

Now, folks, here’s the deal with Apple Vision Pro. It’s this super cool, futuristic tech that’s got everyone buzzing. But, to be honest, we’re not entirely sure how we’re all going to use it just yet. I mean, it’s like having a shiny new tool, and you’re not quite sure what masterpiece you’re going to create with it. But that’s what makes it exciting, right?

Oh, and here’s the kicker – it comes with a price tag of $3500. Now, that might sound like a lot, and it is, but here’s the thing: this is just the beginning. This version of Apple Vision Pro might not be an instant smash hit because it’s still exploring uncharted territory. It’s like the first draft of what could be a great novel or the opening act of an epic movie.

But what’s cool is that it’s laying the groundwork for something truly amazing. It’s like the first brick in what could become an entirely new industry. So, even if it doesn’t take the world by storm right away, it’s setting the stage for a future full of mind-blowing possibilities. So, stay tuned, because the best chapters of this story are yet to come!

Navigating Shifting Tides

Apple is a tech giant and doesn’t have too many weak spots, but Apple is a consumer driven company and is at risk of changing consumer preferences. Now, this isn’t just an Apple thing; it’s something all companies need to worry about but Apple is particularly at risk of changing consumer preferences.

Apple is known for its top-notch products that come with a hefty of a price tag. They’re all about the best quality and cool designs, and they’re not exactly known for being budget-friendly. But as we discussed in the previous section, smart phone technology is maturing and innovation is slowing, so will consumers stop paying premium prices if the technology is not advancing? That’s where Apple could run into problems.

There are a few reasons why people’s preferences might change. First, if the economy takes a nosedive, folks tend to be more careful with their money. They might want to pinch pennies and go for cheaper options. Second, emerging markets around the world are popping up, and these folks might not be able to splurge on pricey Apple products. Finally, there’s open source software, which basically means people want to tinker with their tech and make it their own, which is something Apple has been notoriously guarded against.

Apple is being proactive and has tried to deal with this by making more affordable products, like the iPhone SE and MacBook Air. Plus, they’re making it easier for other clever folks to create apps for their devices, giving you more ways to customize things.

But, here’s the catch – Apple’s still not the cheapest kid on the block, and their world is kinda like a club with a strict bouncer. It’s not very open, so you might not have as much freedom to choose.

In the end, changing consumer preferences is a real worry for Apple, but their products are still as popular as ever and they’re trying to make changes and keep the customer happy. We’ll have to wait and see if they can keep up the good work while the world changes around them.

A Closer Look at AAPL’s Intrinsic Worth

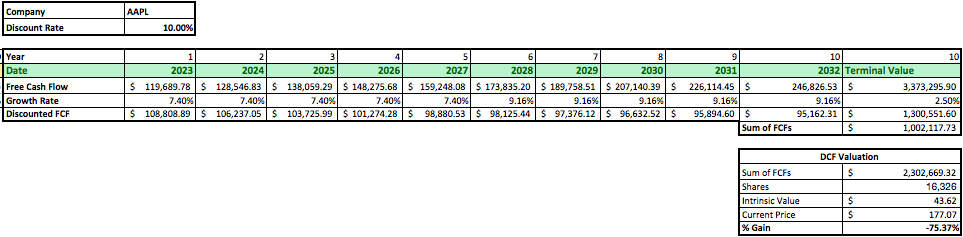

Let’s break down the valuation of Apple Inc., or as we know it, AAPL. Now, we’re doing a little math magic called a discounted cash flow (DCF) analysis. We’ll start with the $111 billion in free cash flow that Apple recorded in 2022.

For the near-term, we’re expecting growth of 7.40% for the next five years based on average analysts growth estimates from Yahoo Finance, therefore we’ll apply an annual growth rate of 7.40% for the first five years of the analysis.

Now, beyond that five-year window, it’s like trying to predict the weather in 2030 – unpredictable! So, we’ll play it safe and use the average compounded revenue and earnings growth rate of the past decade, which stands at 9.16%. We’ll apply this rate from year 6 to year 10 of our DCF analysis.

Our discount rate is 10%, representing the market’s average rate of return with dividends reinvested, and we’re assuming a terminal growth rate of 2.5% for Apple’s cash flows to follow the longterm rate of inflation.

So, after crunching those numbers, we find that Apple’s intrinsic value, the real deal, is about $43.62 per share which represents a potential loss of 75% from it’s current share price. That’s right, Apple’s current stock price is way higher than what we’d call its “true value.”

In plain English, that means Apple might be overvalued. So, before we jump on the Apple bandwagon, let’s remember this: even though Apple’s past performance is impressive, the future might not be as dazzling. We need to be cautious investors.

Wrapping it All Up

Apple Inc., or AAPL, is a tech giant known for rocking the financial charts and having the most loyal fan base. But, as always, a pinch of caution never hurts.

In the past decade, Apple has been on a winning streak, with impressive revenue and cash flow growth. That’s partly thanks to its die-hard customer base, who can’t get enough of Apple’s cool gadgets.

Now, looking ahead to 2023, it’s like a rollercoaster: moderate growth in earnings (1.30%), but a bit of a dip in revenue (-0.90%). But hold onto your seats because 2024 looks exciting with an expected 8.90% growth in earnings and a 6.30% rise in revenue.

Apple is also diversifying its toolkit with amazing stuff like the Apple Vision Pro, changing how we connect with tech. And let’s not forget about those services, like Apple Music and Apple TV+, raking in serious cash.

However, a little cloud on the horizon: changing consumer preferences and open-source trends. Apple’s brand loyalty is still a superpower, but the tech world keeps spinning.

In terms of the numbers, Apple’s stock price might be dancing high above its intrinsic value, signaling a potential overvaluation. So, if you’re thinking of joining the Apple party, just remember to be a savvy investor. Apple’s success is rooted in its fans, diverse product range, and dedication to innovation. Stay cool, and keep those apples coming!

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AAPL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article.

The Pineapple Investor’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The Pineapple Investor is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.