Summary

- Paylocity specializes in payroll and human capital management solutions for small to midsize businesses in the United States.

- We believe PCTY strong growth over the last decade can be attributed to its relentless focus on the employee experience.

- While PCTY has exhibited impressive growth in its revenue, client base, and price return, we must also acknowledge the risks associated with its rapid expansion.

- The projected intrinsic value of PCTY, calculated through our discounted cash flow analysis, comes in at $113.87.

Intro

Paylocity (PCTY) is a company that specializes in providing payroll and human capital management solutions. They mainly serve small to midsize businesses in the United States. Over the years, it has focused on serving companies with a specific range of employees – from as few as 10 to as many as 5,000.

In addition to the core payroll services, PCTY also provides HCM solutions. This includes tools for tracking employee attendance, software to help with recruiting new talent, and even tools for collaboration and communication within the workplace.

In a nutshell, PCTY is all about helping businesses manage their payroll and their people, especially those smaller to midsize companies in the U.S. They’ve come a long way since their founding, and they’re currently serving around 36,000 clients as of the most recent fiscal year in 2023.

In this analysis, we’ll closely examine PCTY’s financial performance and its potential for future growth. Our investigation will delve into the company’s revenue generation, profitability, and its ability in managing cash flow. By gaining a comprehensive understanding of these facets, you’ll be better prepared to make an informed investment decision regarding PCTY, and you’ll also comprehend why we recommend considering an investment in the stock.

Track Record

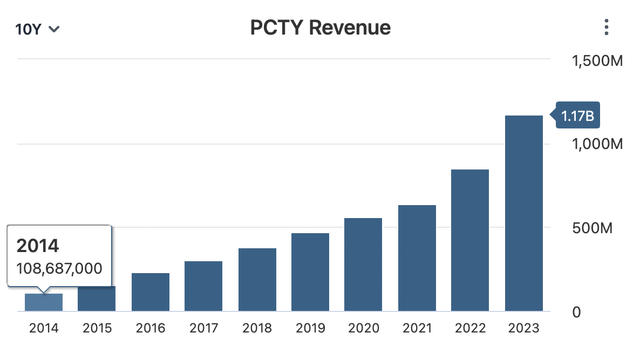

First, we have the top line revenue. Last year, in 2023, PCTY generated $1.75 billion in revenue. If we go back to 2014, they had just $108 million. That’s an impressive total growth of approximately 981% over these ten years. When we calculate the average annual growth rate, it comes out to about 26.88%.

Data by Stock Analysis

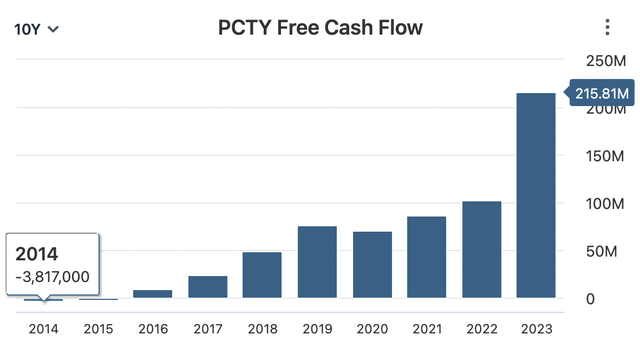

Now, let’s talk about the free cash flow. In 2023, PCTY had $215 million in free cash flow. Going back to 2014, it was in the negative at -$3.82 million. Now, this negative number indicates that PCTY was not a profitable company but since 2016 the company has been gradually growing its free cash flow by a substantial margin ever since.

Data by Stock Analysis

Year-to-year fluctuations in a company’s free cash flow are influenced by various unpredictable factors, including economic conditions, seasonality, unexpected costs, currency fluctuations, regulations, market trends, geopolitical events, and natural disasters. Given this uncertainty, our approach is to understand a company’s core strengths and weaknesses, identifying competitive advantages that enable sustained financial performance. This strategy helps minimize the impact of external, unpredictable forces on our investments.

We believe PCTY strong growth over the last decade can be attributed to its relentless focus on the employee experience. Many older HR systems were mainly designed to help employees complete basic HR tasks but today’s modern workforce, people want more than just transactional HR interactions. PCTY believes employees want to communicate, collaborate, and feel connected to their work.

To meet these needs, PCTY has integrated various features, like video and chat, into their platform. These features aim to create a sense of connection among employees, even if they work remotely, are always on the move, or don’t’ have corporate email addresses.

Now, here’s the key part that sets PCTY apart from the competition: They’re using these employee experiences to enhance their Human Capital Management ((HCM)) platform. This not only makes HR processes more efficient, thanks to employees taking care of things themselves, but it also improves HR teams’ ability to reach and communicate effectively with employees.

In a nutshell, they’re adapting to the changing demands of the modern workforce by making HR more about communication, collaboration, and connection, using technology to help employees feel more engaged with their work. It’s PCTY is putting the human in human resources and it’s translating to substantial top and bottom-line growth.

To assess whether PCTY’s unwavering commitment to the employee experience yields measurable outcomes, let’s analyze its performance relative to other firms in the Human Resources and Employee Services industry. After evaluating 34 companies in this industry, we find that PCTY stands out, securing the 4th position in revenue growth over the past 5 years and also in free cash flow growth over the last 3 years.

This data affirms our belief that PCTY’s competitive edge, rooted in its dedication to enhancing the employee experience, is indeed tangible and propelling the company toward above-average growth within its industry.

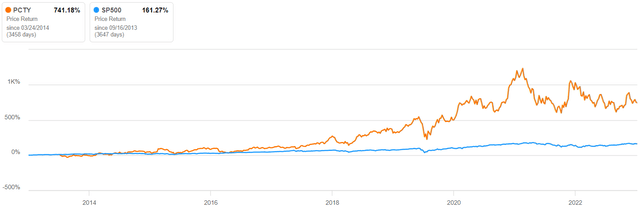

Moreover, PCTY’s strategy has powered the company to an impressive return over the years. In the past 10 years the company is boasting a 741% increase in share price. In contrast, when we look at the broader market, represented by the S&P 500, it had a return of 161% during the same period. However, such outsized performance over the years may cause investors to question whether regression to the mean may be in order for the company’s share price.

Data by Seeking Alpha

Outlook

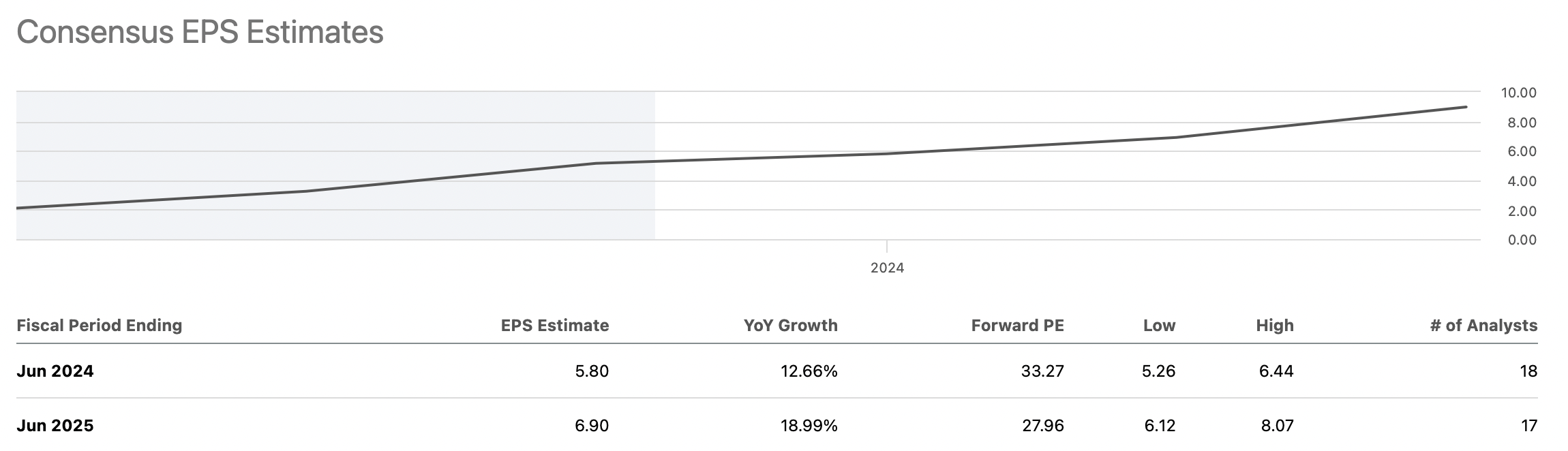

PCTY appears to have a bright future as predicted by the average analyst earnings estimates. Looking ahead to the fiscal year ending in June 2024, analyst estimate earnings per share to be around $5.80. This represents a growth of approximately 12.66% compared to the previous year. If we extend our view to the following fiscal year ending in June 2025, the estimated EPS rises to $6.90, showing an even more significant growth rate of about 18.99% compared to the previous year.

Data by Seeking Alpha

It’s important to approach analyst earnings estimates with a healthy dose of skepticism. While analysts are knowledgeable and well-informed, they don’t possess a crystal ball that predicts the future of a company’s earnings with absolute certainty. Economic, industry, and company-specific factors can be unpredictable, and unforeseen events can impact earnings.

However, this doesn’t mean we should disregard analyst estimates altogether. Instead, we should consider them as valuable tools for gaining a sense of general direction a company is headed in terms of its earnings. They provide a consensus view based on available information and analysis.

We do believe that analyst have a good reason to be optimistic about PCTY. The company is making strides in its product development efforts, and their hard work hasn’t gone unnoticed. They’ve been consistently recognized as an overall leader in all 12 HRIS (Human Resources Information System) product categories for an impressive 15 quarters in a row by G2 Crowd, which is an independent product review site. This recognition suggests that their products are well-regarded by users and experts alike.

Additionally, PCTY has recently announced some new cutting-edge product offerings which we believe point to strong earnings prospects. The new product offerings include the introduction of Market Pay, Advanced Scheduling, improved Learning Management System (LMS), and Generative AI, all of which demonstrate a commitment to redefining modern HR.

The company’s new Market Pay product includes real-time market pay data integration that enhances compensation decisions and compliance, attracting larger enterprises. Advanced Scheduling includes automation, cost reduction, and mobile scheduling which will empower businesses and employees, riding the mobile shift trend.

Also, the LMS Enhancements product has a vast course catalog and content creation capabilities increasing training efficiency, and data shows a 70% course completion boost among employees since July 2022.

Finally, perhaps the most exciting addition to the company’s product offering is Generative AI which involves Innovative AI-driven communication, job description creation, and streamline processes, saving time and improving talent acquisition.

Now, PCTY is also working on expanding its sales team. They’ve been hiring new sales representatives and investing in their referral channel and digital lead generation initiatives. This is all part of their strategy to reach more customers effectively.

In fiscal 2022, they managed to grow their client base by approximately 16%, and they now serve over 33,000 clients. What’s interesting is that they see even more growth potential ahead. They’ve identified over 1.3 million businesses in their target market-organizations with 10 to 5,000 employees. So, they believe there are plenty of opportunities for further growth.

In essence, PCTY is not only earning recognition for its product development efforts by also actively expanding its reach and client base. We believe their focus on innovation and growth indicates their commitment to staying competitive and serving a wider range of organizations.

However, while there are reasons to be optimistic regarding the PCTY’s future, there are some real risks that need to be considered. One of the key risks is the company’s ability to manage its rapid growth effectively. PCTY has experienced significant growth in both revenue and its client base, and they plan to continue this growth as part of their business strategy.

Rapid growth is great however, this growth comes with its challenges. It places substantial demands on the company, requiring increased capital expenditures and higher operating expenses. To handle this growth properly, they need to attract, train, and retain a considerable number of qualified personnel in various roles, such as sales, implementation, client service, software development, information technology, and management.

In addition to personnel, they also need to maintain and enhance their technology infrastructure and financial and accounting systems. Moreover, they rely on a network of third-party service providers, including advisors and consultants, for potential client referrals.

Now, here’s the crux of the matter: If PCTY fails to manage this growth effectively, it could have several adverse consequences. Their expenses might rise more than expected, their revenue could decline, or it might grow more slowly than anticipated. This could, in turn, impact their ability to implement their business strategy and sustain their revenue growth rates. They might also encounter operational mistakes, missed business opportunities, and employee losses.

So, while PCTY’s growth is a positive sign, it’s essential to be aware of the challenges associated with managing such rapid expansion. As potential investors, we should carefully monitor how well they handle these challenges.

Valuation

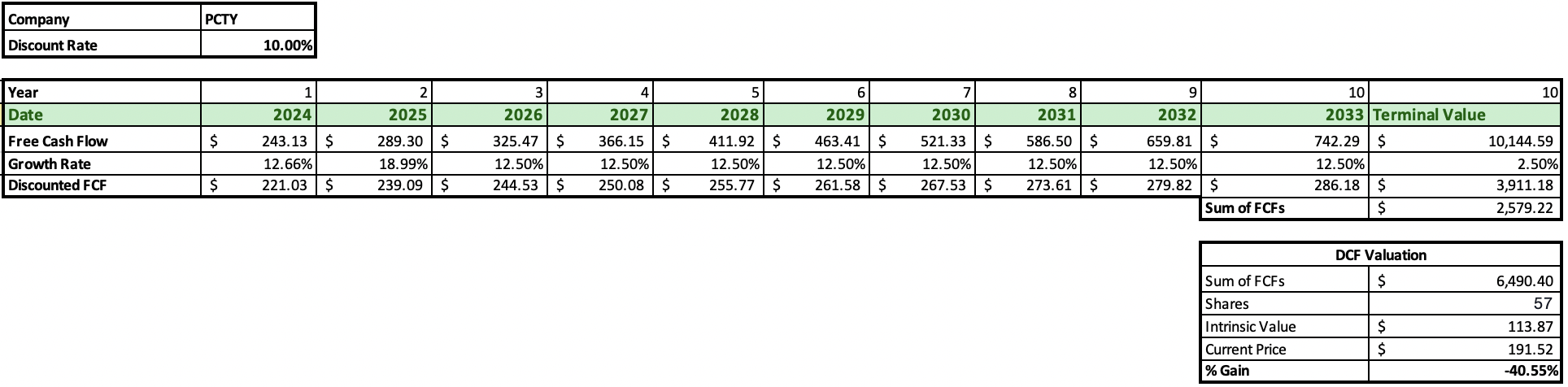

To determine PCTY’s intrinsic value, we’ll employ a discounted cash flow analysis. This approach allows us to estimate the true value of the company’s stock based on its projected future cash flows.

First, we’ll begin with the company’s initial free cash flow in 2023, which amounts to $215.81 million. Now, we need to estimate the growth rate for the upcoming years. Analysts project an increase of 12.66% for 2024 and a more substantial growth rate of 18.99% for 2025.

Moving on to the next phase of our DCF analysis, we typically rely on the average compounded annual growth rate of both revenue and free cash flow over the past decade. However, considering that the growth rate is notably high, over 25%, we’ll opt for a more conservative approach. We’ll apply a growth rate of 12.50% for the subsequent years, specifically from year 3 through year 10.

We firmly believe that these growth rates are well-founded, driven by the company’s expanded sales team, innovative product offerings, and strategic emphasis on enhancing the employee experience.

Now, for our discount rate, we’ll use 10%, which represents the market’s average return with reinvested dividends. Additionally, we need to consider the perpetual growth rate, which signifies how much the company is expected to grow indefinitely after year 10. Here, we’ll use a conservative estimate of 2.5%.

After crunching the numbers, PCTY’s projected intrinsic value comes out to be $113.87. This estimate represents what we believe the stock should be worth based on our analysis, indicating a potential return of -40.55%.

Author’s Work

Takeaway

As we wrap up our analysis of PCTY, let’s consider the big question: Should you buy, hold, or sell this stock based on the current valuation?

The projected intrinsic value of PCTY, calculated through our discounted cash flow analysis, comes in at $113.87. This estimate suggests that the stock may be overvalued compared to its current market price, indicating a potential downside of around -40.55%.

While PCTY has exhibited impressive growth in its revenue, client base, and price return, we must also acknowledge the risks associated with its rapid expansion. Managing such growth effectively can be a formidable challenge, and any missteps could have adverse consequences on the company’s financial performance and ability to execute its business strategy.

Considering the potential downside indicated by our valuation analysis and the challenges related to managing rapid growth, it might be prudent for investors to exercise caution when contemplating an investment in PCTY at its current valuation. Overall, we love company but we’ll wait for a better price.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article.

The Pineapple Investor’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The Pineapple Investor is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.